One of the first steps in analyzing a business transaction is deciding if the accounts involved increase or decrease. However, we do not use the concept of increase or decrease in accounting. We use the words “debit” and “credit” instead of increase or decrease. The meaning of debit and credit will change depending on the account type. Debit simply means left side; credit means right side. Remember the accounting equation? ASSETS = LIABILITIES + EQUITY The accounting equation must always be in balance and the rules of debit and credit enforce this balance.

In each business transaction we record, the total dollar amount of debits must equal the total dollar amount of credits. When we debit one account (or accounts) for $100, we must credit another account (or accounts) for a total of $100. The accounting requirement that each transaction be recorded by an entry that has equal debits and credits is called double-entry procedure, or duality. Watch this video to help you remember this concept:

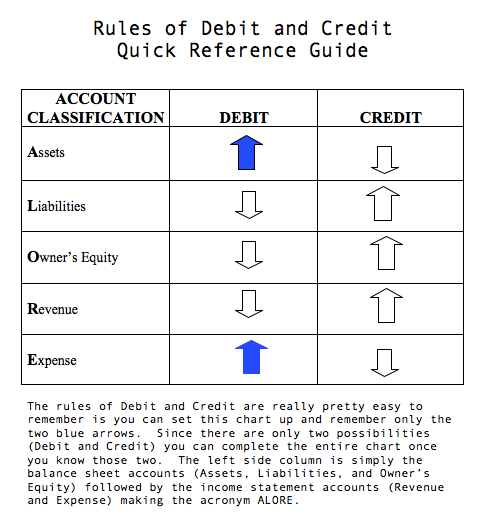

Review this quick guide to recording debits and credits. It will be necessary for you to commit the rules for debits and credits to memory before you move forward in this course. Note: This are general guidelines and we will have exceptions to these rules.

Click Image to Enlarge

After recognizing a business event as a business transaction, we analyze it to determine its increase or decrease effects on the assets, liabilities, stockholders’ equity items, dividends, revenues, or expenses of the business. Then we translate these increase or decrease effects into debits and credits.

Recording Changes in Balance Sheet Accounts

Balance Sheet accounts are assets, liabilities and equity. The balance sheet proves the accounting equation. Recording transactions into journal entries is easier when you focus on the equal sign in the accounting equation. Assets, which are on the left of the equal sign, increase on the left side or DEBIT side. Liabilities and stockholders’ equity, to the right of the equal sign, increase on the right or CREDIT side.

| Assets | Liabilities & Equity |

| DEBIT increases | CREDIT increases |

| CREDIT decreases | DEBIT decreases |

There is an exception to this rule: Dividends (or withdrawals for a non-corporation) is an equity account but it reduces equity since the owner is taking equity from the company. This is called a contra-account because it works opposite the way the account normally works. For Dividends, it would be an equity account but have a normal DEBIT balance (meaning, debit will increase and credit will decrease).

Recording changes in Income Statement Accounts

We learned that net income is added to equity. We also learned that net income is revenues – expenses and calculated on the income statement. The recording rules for revenues and expenses are:

| Revenues | Expenses |

| CREDIT increases | DEBIT increases |

| DEBIT decreases | CREDIT decreases |

The reasoning behind this rule is that revenues increase retained earnings, and increases in retained earnings are recorded on the right side. Expenses decrease retained earnings, and decreases in retained earnings are recorded on the left side.

The side that increases (debit or credit) is referred to as an account’s normal balance. Remember, any account can have both debits and credits. Here is another summary chart of each account type and the normal balances.

| Account Type | Normal Balance |

| Asset | DEBIT |

| Liability | CREDIT |

| Equity | CREDIT |

| Revenue | CREDIT |

| Expense | DEBIT |

| Exception: | |

| Dividends | DEBIT |

Regardless of what elements are present in the business transaction, a journal entry will always have AT least one debit and one credit. You should be able to complete the debit/credit columns of your chart of accounts spreadsheet (click Chart of Accounts).

Next we look at how to apply this concept in journal entries.

Candela Citations

- General Rules for Debits and Credits. Authored by: Jaclyn Strauss. Provided by: Broward College. License: CC BY: Attribution

- Colin Dodds - Debit Credit Theory (Accounting Rap Song). Authored by: Mr. Colin Dodds. Located at: https://youtu.be/j71Kmxv7smk. License: All Rights Reserved. License Terms: Standard YouTube LIcense