What you’ll learn to do: explain production and the production function

Businesses engage in production. What does that mean exactly? What is involved? How is steel production different from growing wheat? In this section, we will begin to learn about the behavior of firms, how they make production decisions, and how production costs depend on a firm’s production function.

Learning Objectives

- Describe and differentiate between the types of inputs in the production process

As we said earlier, this module is the first of several modules that explore the theory of the firm. Let’s define what is meant by the firm. A firm (or business) combines inputs of labor, capital, land, and raw or finished component materials to produce outputs. If the firm is successful, the outputs are more valuable than the inputs. This activity of production goes beyond manufacturing (i.e., making things). It includes any process or service that creates value, including transportation, distribution, wholesale and retail sales. Production involves a number of important decisions that define the behavior of firms. These decisions include, but are not limited to:

- What product or products should the firm produce?

- How should the products be produced (i.e., what production process should be used)?

- How much output should the firm produce?

- What price should the firm charge for its products?

- How much labor should the firm employ?

The answers to these questions depend on the production and cost conditions facing each firm, which is the subject of this module. The answers also depend on the structure of the market for the product(s) in question. Market structure is a multidimensional concept that involves how competitive an industry is. It is defined by questions such as these:

- How much market power does each firm in the industry possess?

- How similar is each firm’s product to the products of other firms in the industry?

- How difficult is it for new firms to enter the industry?

- Do firms compete on the basis of price, advertising, or other product differences?

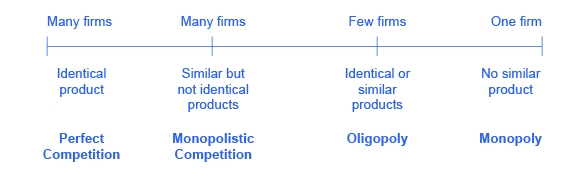

Figure 1 illustrates the range of different market structures, which we will explore in detail in later modules.

Figure 1. The Spectrum of Competition. Firms face different competitive situations. At one extreme—perfect competition—many firms are all trying to sell identical products. At the other extreme—monopoly—only one firm is selling the product, and this firm faces no competition. Monopolistic competition and oligopoly fall between the extremes of perfect competition and monopoly. Monopolistic competition is a situation with many firms selling similar, but not identical, products. Oligopoly is a situation with few firms that sell identical or similar products.

Factors of Production

In this module, we want to explore the relationship between the quantity of output a firm produces, and the cost of producing that output. The cost of the product depends on how many inputs (or factors of production) are required to produce the product and what those inputs cost. We can determine the costs by looking at the firm’s production function, which we will explore in detail in the next section.

Figure 2. The production process for pizza includes inputs such as ingredients, the efforts of the pizza maker, and tools and materials for cooking and serving. (Credit: Haldean Brown/Flickr Creative Commons)

Production is the process (or processes) a firm uses to transform inputs (e.g. labor, capital, raw materials) into outputs, i.e. the goods or services the firm wishes to sell. Consider pizza making. The pizzaiolo (pizza maker) takes flour, water, and yeast to make dough. Similarly, the pizzaiolo may take tomatoes, spices, and water to make pizza sauce. He or she rolls out the dough, brushes on the pizza sauce, and adds cheese and other toppings. The pizzaiolo uses a peel—the shovel-like wooden tool– to put the pizza into the oven to cook. Once baked, the pizza goes into a box (if it’s for takeout) and the customer pays for the good. What are the inputs (or factors of production) in the production process for this pizza?

Economists divide factors of production into several categories:

- Natural Resources (Land and Raw Materials) – The ingredients for the pizza are raw materials. These include the flour, yeast, and water for the dough, the tomatoes, herbs, and water for the sauce, the cheese, and the toppings. If the pizza place uses a wood-burning oven, we would include the wood as a raw material. If the establishment heats the oven with natural gas, we would count this as a raw material. Don’t forget electricity for lights. If, instead of pizza, we were looking at an agricultural product, like wheat, we would include the land the farmer used for crops here.

- Labor – When we talk about production, labor means human effort, both physical and mental. The pizzaiolo was the primary example of labor here. He or she needs to be strong enough to roll out the dough and to insert and retrieve the pizza from the oven, but he or she also needs to know how to make the pizza, how long it cooks in the oven and a myriad of other aspects of pizza-making. The business may also have one or more people to work the counter, take orders, and receive payment.

- Capital – When economists uses the term capital, they do not mean financial capital (money); rather, they mean physical capital, the machines, equipment, and buildings that one uses to produce the product. In the case of pizza, the capital includes the peel, the oven, the building, and any other necessary equipment (for example, tables and chairs).

- Technology – Technology refers to the process or processes for producing the product. How does the pizzaiolo combine ingredients to make pizza? How hot should the oven be? How long should the pizza cook? What is the best oven to use? Gas or wood burning? Should the restaurant make its own dough, sauce, cheese, toppings, or should it buy them?

- Entrepreneurship – Production involves many decisions and much knowledge, even for something as simple as pizza. Who makes those decisions? Ultimately, it is the entrepreneur, the person who creates the business, whose idea it is to combine the inputs to produce the outputs.

The cost of producing pizza (or any output) depends on the amount of labor capital, raw materials, and other inputs required and the price of each input to the entrepreneur.

Try It

Glossary

- factors of production (or inputs):

- resources that firms use to produce their products, for example, labor and capital

- firm:

- an organization that combines inputs of labor, capital, land, and raw or finished component materials to produce outputs.

- production:

- the process of combining inputs to produce outputs, ideally of a value greater than the value of the inputs

Candela Citations

- Modification, adaptation, and original content. Provided by: Lumen Learning. License: CC BY: Attribution

- Introduction to Production. Authored by: Steven Greenlaw and Lumen Learning. License: CC BY: Attribution

- Productive Resources. Provided by: Lumen Learning. Located at: https://courses.lumenlearning.com/wm-macroeconomics/chapter/reading-understanding-economics-and-scarcity/. License: CC BY: Attribution

- Introduction to Production, Costs, and Industry Structure. Provided by: OpenStax College. Located at: https://cnx.org/contents/XAl2LLVA@7.16:SlmDF6TE@7/Introduction-to-Production-Cos. License: CC BY: Attribution. License Terms: Download for free at http://cnx.org/contents/bc498e1f-efe9-43a0-8dea-d3569ad09a82@4.4