Learning Outcomes

- Calculate compound interest given an interest scenario

- Calculate the initial balance given an interest scenario

Compounding

With simple interest, we were assuming that we pocketed the interest when we received it. In a standard bank account, any interest we earn is automatically added to our balance, and we earn interest on that interest in future years. This reinvestment of interest is called compounding.

Suppose that we deposit $1000 in a bank account offering 3% interest, compounded monthly. How will our money grow?

The 3% interest is an annual percentage rate (APR) – the total interest to be paid during the year. Since interest is being paid monthly, each month, we will earn [latex]\frac{3%}{12}[/latex]= 0.25% per month.

In the first month,

- P0 = $1000

- r = 0.0025 (0.25%)

- I = $1000 (0.0025) = $2.50

- A = $1000 + $2.50 = $1002.50

In the first month, we will earn $2.50 in interest, raising our account balance to $1002.50.

In the second month,

- P0 = $1002.50

- I = $1002.50 (0.0025) = $2.51 (rounded)

- A = $1002.50 + $2.51 = $1005.01

Notice that in the second month we earned more interest than we did in the first month. This is because we earned interest not only on the original $1000 we deposited, but we also earned interest on the $2.50 of interest we earned the first month. This is the key advantage that compounding interest gives us.

Calculating out a few more months gives the following:

| Month | Starting balance | Interest earned | Ending Balance |

| 1 | 1000.00 | 2.50 | 1002.50 |

| 2 | 1002.50 | 2.51 | 1005.01 |

| 3 | 1005.01 | 2.51 | 1007.52 |

| 4 | 1007.52 | 2.52 | 1010.04 |

| 5 | 1010.04 | 2.53 | 1012.57 |

| 6 | 1012.57 | 2.53 | 1015.10 |

| 7 | 1015.10 | 2.54 | 1017.64 |

| 8 | 1017.64 | 2.54 | 1020.18 |

| 9 | 1020.18 | 2.55 | 1022.73 |

| 10 | 1022.73 | 2.56 | 1025.29 |

| 11 | 1025.29 | 2.56 | 1027.85 |

| 12 | 1027.85 | 2.57 | 1030.42 |

We want to simplify the process for calculating compounding, because creating a table like the one above is time consuming. Luckily, math is good at giving you ways to take shortcuts. To find an equation to represent this, if Pm represents the amount of money after m months, then we could write the recursive equation:

P0 = $1000

Pm = (1+0.0025)Pm-1

You will see this again in our Algebra, Geometry, and Modeling unit as the recursive form of exponential growth.

recursive growth

Recall the underlying process of recursive growth. From a starting amount, [latex]P_0[/latex], each subsequent amount, [latex]P_m[/latex], grows in proportion to itself, [latex]P_{m-1}[/latex], at some rate [latex]r[/latex].

[latex]P_m=P_{m-1}+r\cdot P_{m-1}[/latex]

Factoring out the [latex]P_{m-1}[/latex] from each term on the right-hand side

[latex]P_m=(1+r)\cdot P_{m-1}[/latex].

In the example below, we’ll build an explicit equation for the growth.

Multiplying terms containing exponents

In the example below, you’ll need to use the rules for multiplying like bases containing exponents

[latex]a^{m}a^{n}=a^{m+n}[/latex].

That is, when multiplying like bases, we add the exponents.

Example

Build an explicit equation for the growth of $1000 deposited in a bank account offering 3% interest, compounded monthly.

View this video for a walkthrough of the concept of compound interest.

While this formula works fine, it is more common to use a formula that involves the number of years, rather than the number of compounding periods. If N is the number of years, then m = N k. Making this change gives us the standard formula for compound interest.

[latex]m=Nk[/latex]

How did we get [latex]m = Nk[/latex]?

Recall that [latex]m[/latex] represents the number of compounding periods that an investment remains in the account, and [latex]k[/latex] represents the number of times per year that your interest is compounded. If your deposit earns interest compounded monthly, then [latex]k = 12[/latex]. If you leave the deposit in for [latex]1[/latex] year, then [latex]m = 12[/latex]. But if [latex]k = 12[/latex] and you leave the deposit in for [latex]2[/latex] years, then [latex]m = 2*12 = 24[/latex]. Looking at that another way, [latex]m = N\text{ years} * k[/latex].

[latex]m = Nk[/latex].

Ex. An investment of $1000 earning interest of 4% compounded quarterly (4 times per year) is left in the account for [latex]3[/latex] years.

We have [latex]4[/latex] compounding periods per year, so [latex]k = 4[/latex]

If we leave our money in for [latex]1[/latex] year, the number of compounding periods is [latex]1*4: m=4[/latex].

If we leave our money in for [latex]3[/latex] years, [latex]m = 3*4[/latex], or [latex]12[/latex].

Knowing that investments are usually left to grow over years than over a number of compounding periods, we’ll adjust the formula slightly and just write [latex]Nk[/latex]. This will make it easier to load the formula into a spreadsheet. See the quantitative reasoning module for more on how to use spreadsheets with financial analysis.

Compound Interest

[latex]P_{N}=P_{0}\left(1+\frac{r}{k}\right)^{Nk}[/latex]

- PN is the balance in the account after N years.

- P0 is the starting balance of the account (also called initial deposit, or principal)

- r is the annual interest rate in decimal form

- k is the number of compounding periods in one year

- If the compounding is done annually (once a year), k = 1.

- If the compounding is done quarterly, k = 4.

- If the compounding is done monthly, k = 12.

- If the compounding is done daily, k = 365.

In the next example, we show how to use the compound interest formula to find the balance on a certificate of deposit after 20 years.

don’t forget to convert percent to a decimal

Usually, in order to perform calculations on a number expressed in percent form, you’ll need to convert it to decimal form. The rate [latex]r[/latex] in interest formulas must be converted from percent to decimal form before you use the formula.

Example

A certificate of deposit (CD) is a savings instrument that many banks offer. It usually gives a higher interest rate, but you cannot access your investment for a specified length of time. Suppose you deposit $3000 in a CD paying 6% interest, compounded monthly. How much will you have in the account after 20 years?

A video walkthrough of this example problem is available below.

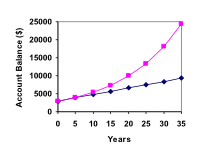

Let us compare the amount of money earned from compounding against the amount you would earn from simple interest

| Years | Simple Interest ($15 per month) | 6% compounded monthly = 0.5% each month. |

| 5 | $3900 | $4046.55 |

| 10 | $4800 | $5458.19 |

| 15 | $5700 | $7362.28 |

| 20 | $6600 | $9930.61 |

| 25 | $7500 | $13394.91 |

| 30 | $8400 | $18067.73 |

| 35 | $9300 | $24370.65 |

As you can see, over a long period of time, compounding makes a large difference in the account balance. We will see this again as the difference between linear growth and exponential growth.

Linear growth vs exponential growth

Linear growth increases at a constant rate. A graph of linear growth will describe a straight line between any two points on the graph. The graph changes by the same additive amount per unit of input.

For example, a bank account that grows at $5 per year experiences linear growth.

Exponential growth describes a quantity growing at a rate proportional to itself for each unit of input. The graph changes by a multiple of its current value per unit of input. The graph will describe a quickly rising curve.

For example, an account that grows at 2% per year experiences exponential growth.

Try It

Evaluating exponents on the calculator

When we need to calculate something like [latex]5^3[/latex] it is easy enough to just multiply [latex]5\cdot{5}\cdot{5}=125[/latex]. But when we need to calculate something like [latex]1.005^{240}[/latex], it would be very tedious to calculate this by multiplying [latex]1.005[/latex] by itself [latex]240[/latex] times! So to make things easier, we can harness the power of our scientific calculators.

Most scientific calculators have a button for exponents. It is typically either labeled like:

^ , [latex]y^x[/latex] , or [latex]x^y[/latex] .

To evaluate [latex]1.005^{240}[/latex] we’d type [latex]1.005[/latex] ^ [latex]240[/latex], or [latex]1.005 \space{y^{x}}\space 240[/latex]. Try it out – you should get something around 3.3102044758.

Example

You know that you will need $40,000 for your child’s education in 18 years. If your account earns 4% compounded quarterly, how much would you need to deposit now to reach your goal?

Try It

Rounding

It is important to be very careful about rounding when calculating things with exponents. In general, you want to keep as many decimals during calculations as you can. It is even better to avoid rounding at all until the final step. This can, however, be tricky to do in a calculator.

Example

To see why not over-rounding is so important, suppose you were investing $1000 at 5% interest compounded monthly for 30 years.

| P0 = $1000 | the initial deposit |

| r = 0.05 | 5% |

| k = 12 | 12 months in 1 year |

| N = 30 | since we’re looking for the amount after 30 years |

If we first compute r/k, we find 0.05/12 = 0.00416666666667

Here is the effect of rounding this to different values:

| r/k rounded to: | Gives P30 to be: | Error |

| 0.004 | $4208.59 | $259.15 |

| 0.0042 | $4521.45 | $53.71 |

| 0.00417 | $4473.09 | $5.35 |

| 0.004167 | $4468.28 | $0.54 |

| 0.0041667 | $4467.80 | $0.06 |

| no rounding | $4467.74 |

Ideally, we wouldn’t round at all. Notice that even rounding to seven decimal places left our final answer off by 6 cents. Rounding to only five decimal places made us miss the correct amount by over $5. This is too far off. And this happened with only $1000 invested. Imagine how far off we could have been with $10,000 or $50,000!

View the following for a demonstration of this example (UPDATE THIS ONE).

Using your calculator

In many cases, you can avoid rounding completely by how you enter things in your calculator. For example, in the example above, we needed to calculate [latex]{{P}_{30}}=1000{{\left(1+\frac{0.05}{12}\right)}^{12\times30}}[/latex]

We can quickly calculate 12×30 = 360, giving [latex]{{P}_{30}}=1000{{\left(1+\frac{0.05}{12}\right)}^{360}}[/latex].

Now we can use the calculator.

| Type this | Calculator shows |

| 0.05 ÷ 12 = . | 0.00416666666667 |

| + 1 = . | 1.00416666666667 |

| ^ 360 = . | 4.46774431400613 |

| × 1000 = . | 4467.74431400613 |

Using your calculator continued

The previous steps were assuming you have a “one operation at a time” calculator; a more advanced calculator will often allow you to type in the entire expression to be evaluated. If you have a calculator like this, you will probably just need to enter:

1000 × ( 1 + 0.05 ÷ 12 ) ^ 360 =

This is the end of the section. Close this tab and proceed to the corresponding assignment.

Candela Citations

- Question ID 6692. Authored by: Lippman,David. License: CC BY: Attribution. License Terms: IMathAS Community License CC-BY + GPL

- Revision and Adaptation. Provided by: Lumen Learning. License: CC BY: Attribution

- Math in Society. Authored by: Open Textbook Store, Transition Math Project, and the Open Course Library. Located at: http://www.opentextbookstore.com/mathinsociety/. License: CC BY-SA: Attribution-ShareAlike

- achievement-bar-business-chart-18134. Authored by: PublicDomainPictures. Located at: https://pixabay.com/en/achievement-bar-business-chart-18134/. License: CC0: No Rights Reserved

- Compound Interest. Authored by: OCLPhase2's channel. Located at: https://youtu.be/xuQTFmP9nNg. License: CC BY: Attribution

- Compound interest CD example. Authored by: OCLPhase2's channel. Located at: https://youtu.be/8NazxAjhpJw. License: CC BY: Attribution

- Compound interest - the importance of rounding. Authored by: OCLPhase2's channel. Located at: https://youtu.be/VhhYtaMN6mo. License: CC BY: Attribution

- Question ID 6693. Authored by: Lippman,David. License: CC BY: Attribution. License Terms: IMathAS Community License CC-BY + GPL