Learning Outcomes

- Record direct materials and direct labor for a job

In this section, you’ll be assigning direct material and direct labor costs to a job.

So far, MaBoards has accumulated the following costs:

| Debit | Credit |

|---|---|

| 150,000 | |

| 2,500 | |

| Double line 147,500 | Double line |

| Debit | Credit |

|---|---|

| 150,000 | |

| Double line | Double line150,000 |

| Debit | Credit |

|---|---|

| 2,500 | |

| Double line 2,500 | Double line |

DIRECT MATERIALS INVENTORY

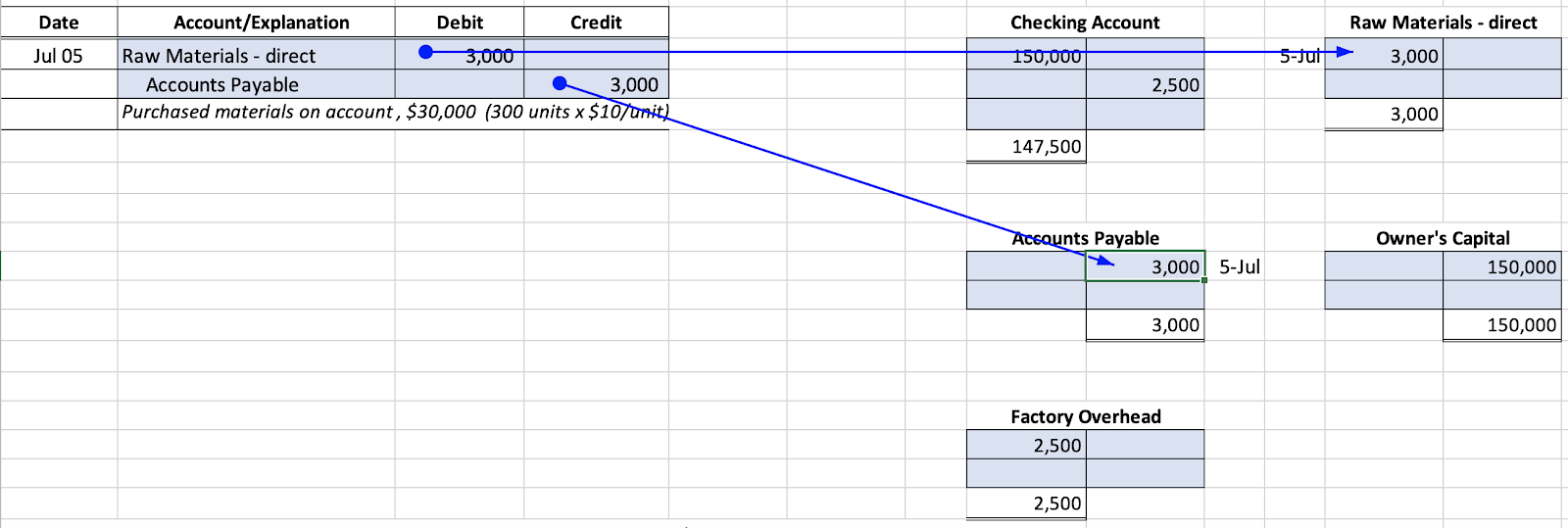

On July 5th, Jackie purchased enough wood for 60 skateboards from a local supplier who has agreed to let her pay the $3,000 bill within 30 days with no interest. She journalized the entry like this:

| Date | Account/Explanation | Debit | Credit |

|---|---|---|---|

| Jul 05 | Raw Materials – direct | 3,000 | |

| Accounts Payable | 3,000 | ||

| Purchased materials on account, $3,000 (60 units x $50/unit) |

Accounts Payable is a liability account that represents bills that are due for purchases and other costs of doing business, and the Raw Materials account is an asset that represents materials on hand.

As she posted the transaction to the ledger, she created a new account for Raw Materials that would be used directly to make boards, and a new account to track bills that she had to pay (Accounts Payable).

The general ledger now appears as follows:

The accounting equation is still in balance, proving that debits = credits:

147,500 + 3000 = 3000 + 150,000 – 2,500

Another way to show this is called a trial balance:

| DR | CR | |

|---|---|---|

| Checking Account | 147,500 | |

| Raw Materials – direct | 3,000 | |

| Accounts Payable | 3,000 | |

| Owner’s Capital | 150,000 | |

| Factory Overhead | 2,500 | |

| Single Line 153,000Double line | Single Line 153,000Double line |

INDIRECT MATERIALS INVENTORY (Manufacturing supplies)

On the 10th of July, Jackie purchased supplies, like paint and graphics and lacquer, that would be used during production but can’t be traced directly to any particular job. She agreed to pay $1,000 within 30 days.

| Date | Account/Explanation | Debit | Credit |

|---|---|---|---|

| Jul 10 | Raw Materials – indirect | 1,000 | |

| Accounts Payable | 1,000 | ||

| Purchased materials on account. |

After posting the transactions to the ledger, her accounts show the following balances:

From now on, Jackie won’t run a trial balance check every time she posts. She’ll wait until the end of the month.

ESTABLISHING A JOB ORDER

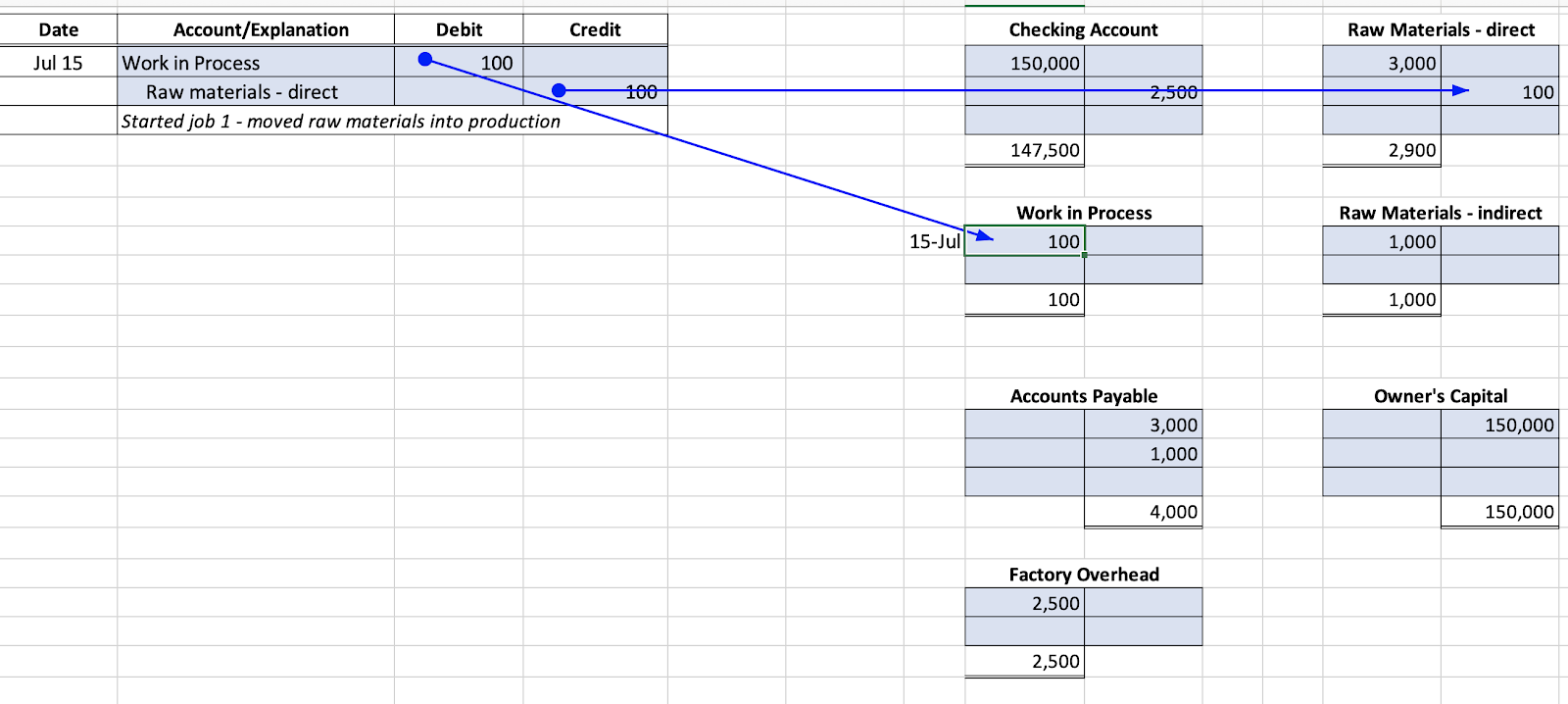

On July 15th, she received an order from Dhanila Parboteeah for a custom skateboard built to her detailed specifications. She has agreed to pay $2,000 for it. Jackie took two units of wood out of storage and placed them on the workbench and started a job card, which is a form that she will use to track direct and indirect costs of the project. She labels Parboteeah’s order as “Job 1” and will track it from now on that way.

| Job Sheet | Job 1 | |

|---|---|---|

| Subcategory, Direct Materials | ||

| Wood | 100 | |

| Wheels and trucks | ||

| Direct Labor | ||

| Overhead allocation | ||

| Total Job Cost | Single Line100Double line | |

She also made the following journal entry:

| Date | Account/Explanation | Debit | Credit |

|---|---|---|---|

| Jul 15 | Work in Process | 100 | |

| Raw materials – direct | 100 | ||

| Started job 1 – moved raw materials into production |

DIRECT MATERIALS ADDED TO JOB

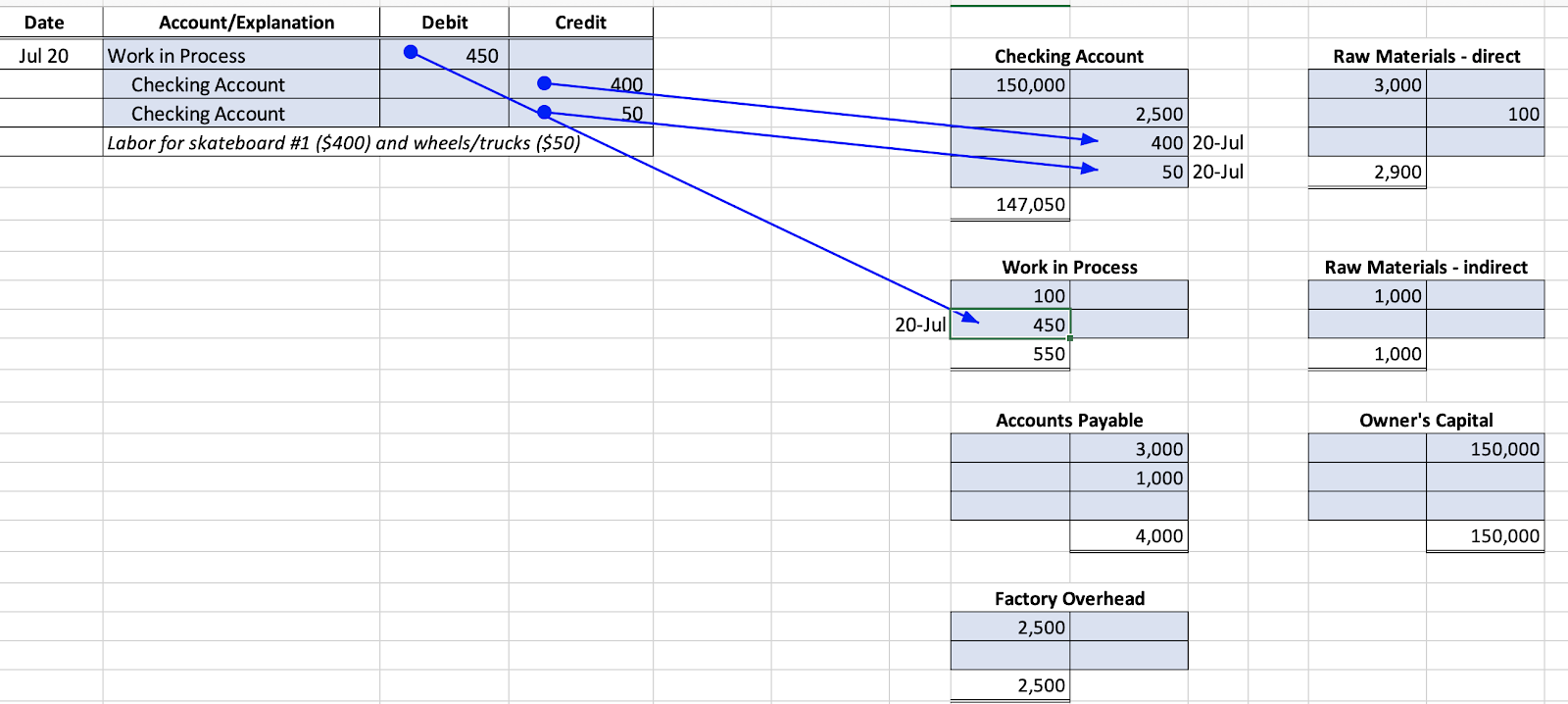

Between the 15th and the 20th, Jackie paid a college student $400 to shape and finish the board. The final touch was installing the trucks and wheels that Jackie purchased online for $50. Since she uses a just-in-time system for the hardware, she doesn’t keep a raw materials inventory account for them. She adds the direct labor and additional materials to both the Work In Process ledger account and the job card.

| Date | Account/Explanation | Debit | Credit |

|---|---|---|---|

| Jul 20 | Work in Process | 450 | |

| Checking Account | 400 | ||

| Checking Account | 50 | ||

| Labor for skateboard #1 ($400) and wheels/trucks ($50) |

| Job Sheet | Job 1 |

|---|---|

| Subcategory, Direct Materials | |

| Wood | 100 |

| Wheels/trucks | 50 |

| Direct Labor | 400 |

| Overhead allocation | |

| Total Job Cost | Single Line550Double line |

The general ledger for MaBoards now looks like this:

Notice the job card shows $550 and is the detail that supports the ledger account called Work in Process.

NEW JOB STARTED

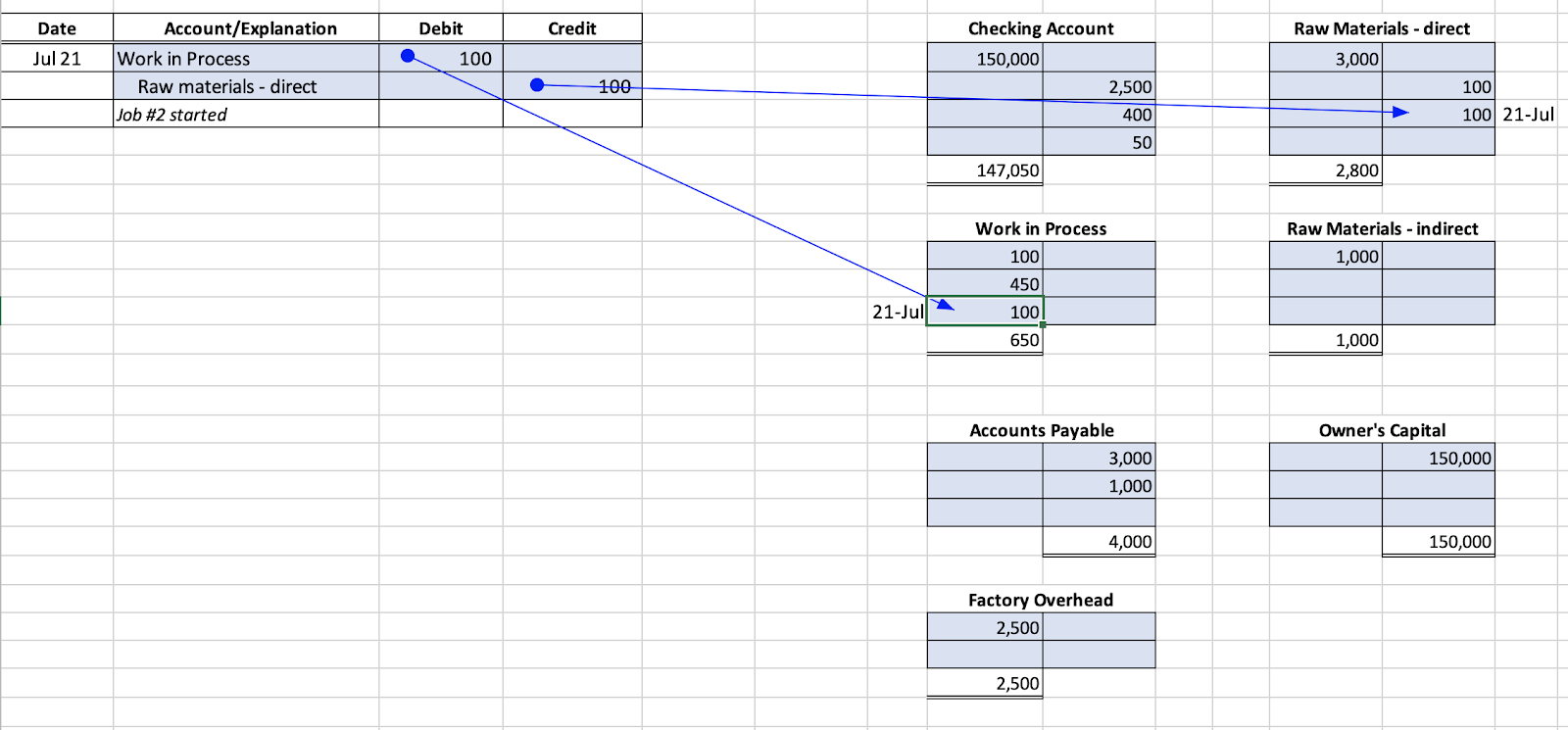

On July 21, Jackie decided to make a custom board to her own specifications to sell online. She put it into production with two units of wood from the supply room. She made a journal entry and started a new job card (#2).

| Date | Account/Explanation | Debit | Credit |

|---|---|---|---|

| Jul 21 | Work in Process | 100 | |

| Raw Materials – direct | 100 | ||

| Job #2 started |

| Job Sheet | Job 1 | Job 2 | Total WIP |

|---|---|---|---|

| Subcategory, Direct Materials | |||

| Wood | 100 | 100 | 200 |

| Wheels/trucks | 50 | 50 | |

| Direct Labor | 400 | 400 | |

| Overhead allocation | 0 | ||

| Total Job Cost | Single Line550Double line | Single Line100Double line | Single Line650Double line |

Notice again that the total of the job cards matches the ledger account called Work in Process. This will always be true. Work in Process is a “control” account that accumulates costs chronologically. The Job Cards serve as a “subsidiary” ledger that sorts those same costs by project.

On July 25th, Jackie purchased deluxe trucks and wheels for $100 for Job 2 and paid her worker $600 for completing the job. She made the journal entry, posted it to the ledger, and updated the job card.

| Date | Account/Explanation | Debit | Credit |

|---|---|---|---|

| Jul 25 | Work in Process | 700 | |

| Checking Account | 600 | ||

| Checking Account | 100 | ||

| Labor for skateboard #2 ($600) and wheels/trucks ($100) |

| Job Sheet | Job 1 | Job 2 | Total WIP |

|---|---|---|---|

| Subcategory, Direct Materials | |||

| Wood | 100 | 100 | 200 |

| Wheels/trucks | 50 | 100 | 150 |

| Direct Labor | 400 | 600 | 1000 |

| Overhead allocation | 0 | ||

| Total Job Cost | Single Line550Double line | Single Line800Double line | Single Line1350Double line |

After posting, the relevant part of the general ledger looks like this (just the Checking Account and Work in Process are shown):

Do the job cards match the Work in Process account?

NEW JOB ORDER

On July 26, Jackie received an order from Xia Zang for a skateboard so she put it into production as Job 3:

| Date | Account/Explanation | Debit | Credit |

|---|---|---|---|

| Jul 26 | Work in Process | 100 | |

| Raw materials – direct | 100 | ||

| Job #3 started |

| Job Sheet | Job 1 | Job 2 | Job 3 | Total WIP |

|---|---|---|---|---|

| Subcategory, Direct Materials | ||||

| Wood | 100 | 100 | 100 | 300 |

| Wheels/trucks | 50 | 100 | 150 | |

| Direct Labor | 400 | 600 | 1000 | |

| Overhead allocation | 0 | |||

| Total Job Cost | Single Line550Double line | Single Line800Double line | Single Line100Double line | Single Line1450Double line |

After posting, the relevant part of the general ledger looks like this (just the direct Raw Materials and Work in Process accounts are shown):

What you may have noticed on the job cards so far is that we haven’t allocated any indirect factory overhead yet. Before we do that, let’s check your understanding of allocating direct costs to jobs.

Practice Question

Candela Citations

- Direct Costs. Authored by: Joseph Cooke. Provided by: Lumen Learning. License: CC BY: Attribution

- Job costing inventory flowchart. Provided by: Lumen Learning. License: CC BY: Attribution