Learning Outcomes

- Adjust for over and under-allocated overhead

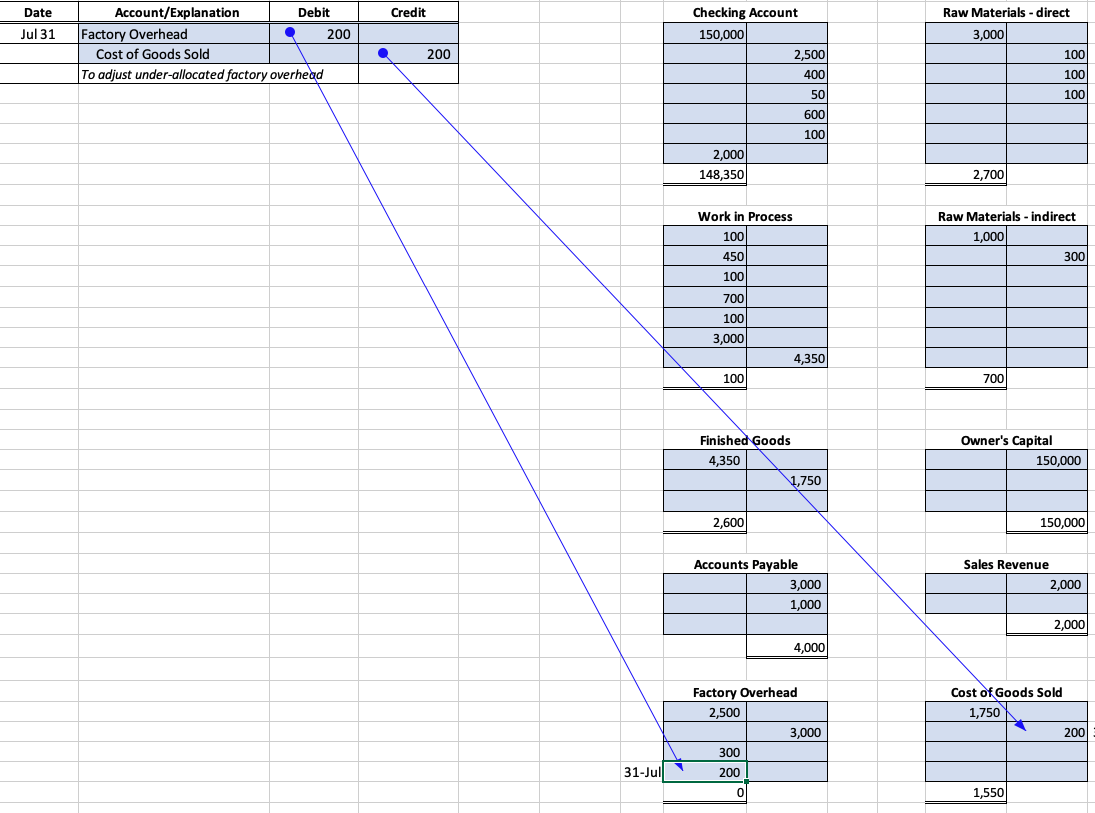

At the end of the month, Jackie notices that her Factory Overhead account looks like this:

| Debit | Credit |

|---|---|

| 2,500 | |

| 3,000 | |

| 300 | |

| Double line | Double line200 |

She used a standard rate to allocate Factory Overhead to jobs during the month that assigned $3,000 of overhead based on $3 per direct labor dollars:

| Job Sheet | Job 1 | Job 2 | Job 3 | Total WIP |

|---|---|---|---|---|

| Subcategory, Direct Materials | ||||

| Wood | 100 | 100 | 100 | 300 |

| Wheels/trucks | 50 | 100 | 150 | |

| Direct Labor | 400 | 600 | 1000 | |

| Overhead allocation ($3/DL$) | 1200 | 1800 | 0 | 3000 |

| Total Job Cost | Single Line1750Double line | Single Line2600Double line | Single Line100Double line | Single Line4450Double line |

Actual overhead was $2,800 ($2,500 rent and $300 materials).

Therefore, the Factory Overhead account shows a credit balance of $200, which means it was over-allocated. In order to reconcile that account, the financial accountants would make the following journal entry:

| Date | Account/Explanation | Debit | Credit |

|---|---|---|---|

| Jul 31 | Factory Overhead | 200 | |

| Cost of Goods Sold | 200 | ||

| To adjust over-allocated factory overhead |

Finally, Jackie will run a trial balance to make sure all debits equal credits and to summarize the accounts as follows:

| DR | CR | Notes | |

|---|---|---|---|

| Checking Account | 148,350 |

|

|

| Raw Materials – direct | 2,700 |

|

|

| Raw Materials – indirect | 700 |

|

|

| Work in Process | 100 |

|

|

| Finished Goods | 2,600 |

|

|

| Accounts Payable | 4,000 |

|

|

| Owner’s Capital | 150,000 |

|

|

| Sales Revenue | 2,000 |

|

|

| Cost of Goods Sold | 1,550 |

|

|

| Factory Overhead | – |

|

|

| Single Line 156,000Double line | Single Line 156,000Double line |

We can see that after accounting for the overhead which was over-allocated to Jobs 1 and 2 by recording it as an adjustment to Cost of Goods Sold, it improves MaBoards financial gross profit by $200. As long as those final adjustments are not material to the financial statements taken as a whole, managerial accountants feel that the additional benefit of having real-time information makes up for the lack of precision that comes with estimating Factory Overhead by using a standard rate during the month.

Instead of plugging under or overallocated overhead into cost of goods sold as an unassigned

(to any job) amount, we could re-allocate factory overhead to jobs based on the actual amount of overhead incurred, but that would be of more interest to financial accountants who are focused on historical data.

Obviously, the managerial accountants will adjust the rate based on historical and projected information.

Watch this video to see how to dispose of overallocated or under-allocated overhead.

You can view the transcript for “Underapplied or Overapplied Manufacturing Overhead (how to dispose of it)” here (opens in new window).

Now, let’s check your understanding of adjusting Factory Overhead at the end of the month.

Practice Question

Candela Citations

- Introduction to Month-end Reporting. Authored by: Joseph Cooke. Provided by: Lumen Learning. License: CC BY: Attribution