Learning Outcomes

- Prepare a production cost report for the first stage of a multi-step process using the weighted-average method

There are two basic methods used to allocate costs in process costing: weighted average and First-in, First-out (FIFO).

For now, we’ll focus on the weighted average method which assumes that products and therefore costs, flow through the process like paint or beverages. Later, once you are comfortable with the basic idea of the process costing production report, we’ll take a look at the FIFO method which is based on the assumption that the work-in-process sitting in the department at the end of the month is finished at the beginning of the next month before anything else is started.

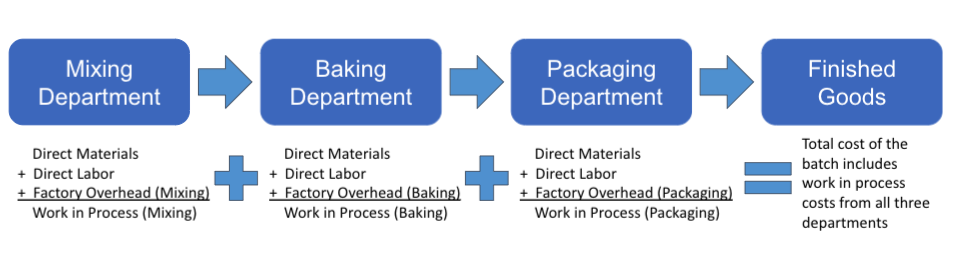

Allocating Costs to Products in the First Department of a Multi-Step Process

What we are looking at here is a multi-step process, such as creating food products. In our Dad’s Perfect Pie (crusts) example, the 3 steps to get from raw materials (flour and butter) to a finished product probably look like this, and so these would be our cost accounting departments as well:

Let’s assume a ton of flour and ¾ ton of butter comes into the Mixing Department on Jan 3rd. A ton of flour makes 3,000 pie crusts. It is mixed up, rolled out, and cut into shape by machine, so there are minimal direct labor costs and some indirect factory overhead costs (such as depreciation, rent, insurance, indirect labor) added to the direct materials costs.

Here is how the production schedule looked:

- Jan 6: 500 pounds of flour and 375 pounds of butter turned into 750 pie crusts (uncooked) and transferred to Baking on Jan 14

- Jan 15: 500 pounds of flour and 375 pounds of butter turned into 750 pie crusts (uncooked) and transferred to Baking on Jan 20

- Jan 21: 500 pounds of flour and 375 pounds of butter turned into 750 pie crusts (uncooked) and transferred to Baking on Jan 27

- Jan 28: 500 pounds of flour and 375 pounds of butter dumped into the mixing process – 60% mixed as of Jan 31

In our accounting records, we shouldn’t transfer all of the direct material costs into baking. Instead, we should leave those unmixed raw materials in the Mixing Department work in process and only transfer out the costs attributed to the product transferred out.

Here are the costs for the mixing department for January:

Direct materials:

1 ton flour at $0.60 per pound = $1,200

¾ ton butter at $1.20 per pound = $1,800

Total Direct Materials = $3,000

Conversion costs:

90 hours direct Labor at $20/hr = $1,800

3,600 machine hours at $0.40/DMH = $1,440

Total Conversion costs: $3,240

Total costs that need to be allocated = $6,240

If we just divided $6,240 by 3,000 crusts we would get $2.08 per crust, but recall that 750 of those shells are not done yet, so they should not get a full allocation of the conversion costs.

We completed and transferred out 3 batches of 750 crusts. That’s 2,250 shells transferred to baking, but once again, we can’t take total costs of $6,240 and allocate that cost over only the completed shells, because $750 of that $6,240 is direct materials in work-in-process, and some of the indirect costs should stay in the mixing department work-in-process as well.

This is where equivalent units come in.

A unit that is 60% done is the equivalent of 6/10 of a completed unit. So, the 750 pie crusts in process on Jan 31 would be, for conversion cost purposes, the equivalent of 450 completed units. For direct materials cost purposes, those units are 100% complete because all of the direct materials are added at the very beginning of the process.

| Equivalent Units – used to allocate | |||

|---|---|---|---|

| Date | Direct Materials | Direct Labor and Overhead | Single LineStatus |

| 3-Jan | Single Line 750 | Single Line 750 | Single Linecompleted and transferred to baking |

| 15-Jan | 750 | 750 | completed and transferred to baking |

| 21-Jan | 750 | 750 | completed and transferred to baking |

| 28-Jan | 750 | 450 | mixing department work-in-process |

| Single Line3,000Double line | Single Line2,700Double line |

Again, the 750 units in work-in-process are 100% complete as to direct materials and 60% complete as to other costs, so the EUs are:

750 * 1.00 = 750 equivalents units for direct materials allocation

750 * 0.60 = 450 equivalent units for labor and other conversion costs allocation

In order to document our allocation of costs, we’ll create a Department Production Cost Report in four steps:

Step 1 – Calculate Units to Account For

Establish the total inventory in production by adding units started into production to beginning work in process (what was left only partially finished at the end of the prior month). For this example, we will assume that all pie shells in process were completed in December and the facility was shut down over the holiday break for the annual repairs, maintenance, and deep clean. So, the beginning inventory of zero plus the 3,000 pie shells worth of materials placed into production during the month gives us 3,000 total units to account for.

| UNITS | Physical Units |

|---|---|

| Subcategory, Units to account for: | Single Line |

| Beginning work-in-process | 0 |

| Started in production | 3,000 |

| Total units to account for | Single Line3,000Double line |

Step 2 – Calculate Units Accounted For

The units are then broken down into two categories: direct materials and conversion costs. Units that have been transferred out are 100% complete, so the Equivalent Units and the actual physical units are the same. However, unfinished units (work-in-process) in this department have to be converted to Equivalent Units. In this case, since materials are all added at the beginning (which may not always be the case), the Equivalent Units for Direct Materials is 100% of the actual units, but the Equivalent Units for the Conversion Costs allocation are 60% of actual units or 450 EUs.

| Equivalent Units | |||

|---|---|---|---|

| Physical Units | Single LineDirect Materials | Single LineConversion Costs | |

| Subcategory, Units accounted for: | Single Line | Single Line | Single Line |

| Completed and transferred out | 2,250 | 2,250 | 2,250 |

| Ending work-in-process | 750 | 750 | 450 |

| Total units accounted for | Single Line3,000Double line | Single Line3,000Double line | Single Line2,700Double line |

Total Equivalent Units (also called Equivalent Units of Production or EUPs) is 3,000 for Direct Materials but only 2,700 for Conversion Costs.

Step 3 – Divide Total Costs by Equivalent Units

From the accounting records, we see that total direct materials transferred in to the mixing department was $3,000, and direct labor and manufacturing overhead totaled $3,240. We divided those amounts by the related Equivalent Units to come up with a cost per EU.

| Direct Materials | Conversion Costs | Total Costs | |

|---|---|---|---|

| Subcategory, Costs to account for: | |||

| Beginning work-in-process | $ – | $ – | $ – |

| Costs added during the period | $ 3,000 | $ 3,240 | $ 6,240 |

| Total costs to account for | Single Line$ 3,000 | Single Line$ 3,240 | Single Line$ 6,240Double line |

| Divided by: Total EUP | 3,000 | 2,700 | |

| Cost per equivalent unit | Single Line$ 1.00Double line | Single Line$ 1.20Double line | |

Step 4 – Allocate Costs Based on Equivalent Units

Refer back to step 2:

| Equivalent Units | |||

|---|---|---|---|

| Physical Units | Single LineDirect Materials | Single LineConversion Costs | |

| Subcategory, Units accounted for: | Single Line | Single Line | Single Line |

| Completed and transferred out | 2,250 | 2,250 | 2,250 |

| Ending work-in-process | 750 | 750 | 450 |

| Total units accounted for | Single Line3,000Double line | Single Line3,000Double line | Single Line2,700Double line |

Multiply the cost per equivalent unit by the number of equivalent units for each category of units accounted for.

| Direct Materials | Conversion Costs | Total Costs | |

|---|---|---|---|

| Equivalent units completed and transferred out | 2,250 | 2,250 | |

| Cost per equivalent unit | $ 1.00 | $ 1.20 | |

| Cost allocated to completed units | Single Line$ 2,250Double line | Single Line$ 2,700Double line | Single Line$ 4,950Double line |

| Equivalent units not yet completed | 750 | 450 | |

| Cost per equivalent unit | $ 1.00 | $ 1.20 | |

| Cost allocated to work-in-process | Single Line$ 750Double line | Single Line$ 540Double line | Single Line$ 1,290Double line |

Complete the Production Report

| Equivalent Units | ||||

|---|---|---|---|---|

| UNITS | Physical Units | Single LineDirect Materials | Single LineConversion Costs | |

| Subcategory, Units to account for: | Single Line | Single Line | Single Line | |

| Beginning work-in-process | 0 | |||

| Started in production | 3,000 | |||

| Total units to account for | Single Line3,000Double line | |||

| Subcategory, Units accounted for: | ||||

| Completed and transferred out | 2,250 | 2,250 | 2,250 | |

| Ending work-in-process | 750 | 750 | 450 | |

| Total units accounted for | Single Line3,000Double line | Single Line3,000Double line | Single Line2,700Double line | |

| COSTS | Direct Materials | Conversion Costs | Total Costs | |

| Subcategory, Costs to account for: | ||||

| Beginning work-in-process | $ – | $ – | $ – | |

| Costs added during the period | $ 3,000 | $ 3,240 | $ 6,240 | |

| Total costs to account for | Single Line$ 3,000 | Single Line$ 3,240 | Single Line$ 6,240Double line | |

| Divided by: Total EUP | 3,000 | 2,700 | ||

| Cost per equivalent unit | Single Line$ 1.00Double line | Single Line$ 1.20Double line | ||

| Subcategory, Costs accounted for: | ||||

| Completed and transferred out | $ 2,250 | $ 2,700 | $ 4,950 | |

| Ending work-in-process | $ 750 | $ 540 | $ 1,290 | |

| Total costs accounted for | Single Line$ 3,000Double line | Single Line$ 3,240Double line | Single Line$ 6,240Double line | |

In summary, (1) identify total units for the department, (2) calculate equivalent units for both completed items (transferred out) and uncompleted (work-in-process), (3) divide total costs by total equivalent units to get an allocation rate, (4) multiply the rate from step 3 by the equivalent units in order to allocate total costs to completed items and work-in process.

Before we look at the next department in line, check your understanding of how to allocate process costs to the first department using a weighted average method.

Practice Question

Candela Citations

- Production Report - First Department - Weighted Average. Authored by: Joseph Cooke. Provided by: Lumen Learning. License: CC BY: Attribution

- Pie crust. Provided by: Unsplash. Located at: https://unsplash.com/photos/m-dhIU1gJHM. License: CC0: No Rights Reserved