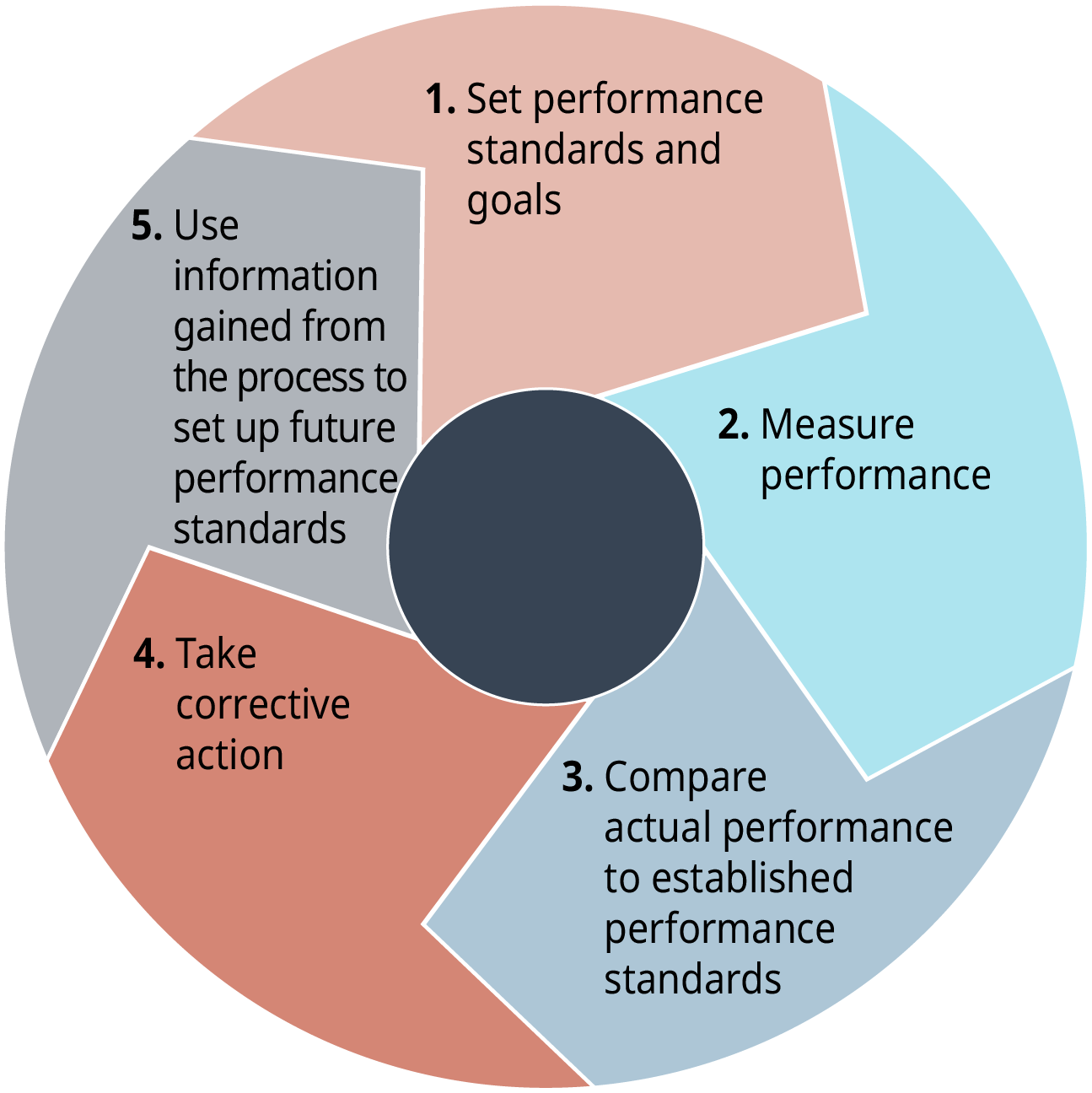

Managing performance can be visualized as a circle encompassing 5 steps:

- Set performance standards and goals

- Using Key Performance Indicators that align with and promote the organizations larger goals and objectives

- There are leading and lagging indicators

- Leading indicators provide information that can be acted upon and that can change results

- Lagging indicators only show historical results

- Measure performance

- KPIs should be based on controllable items for each kind of responsibility center

- For instance, for a revenue center that is based on sales, a KPI could be the number of sales calls made

- The purchasing department may be held accountable for negotiating the best price and measured against standard costs

- The production department may be held accountable for cost overruns due to waste measured by standard volumes

- Net income is a lagging indicator of financial performance

- KPIs should be based on controllable items for each kind of responsibility center

- Compare actual performance to established performance standards

- Management communicates KPIs to responsibility centers, departments, and other managers

- Each KPI should have a benchmark, target, or goal

- Management communicates KPIs to responsibility centers, departments, and other managers

- Take corrective action

- Managers should be held accountable for the costs and performance measures that they can control

- For example, the sales manager can control the number of calls made but not the price that competitors are charging

- Managers should be held accountable for the costs and performance measures that they can control

- Use information gained from the process to set up future performance standards

- Setting KPIs is an iterative process, and should be constantly reviewed for effectiveness.

Finally, here is a quick overview of the concept:

You can view the transcript for “Responsibility Accounting” here (opens in new window).

Or a longer overview here:

You can view the transcript for “Performance Evaluation and Responsibility Centers” here (opens in new window).

Candela Citations

CC licensed content, Original

- Putting It Together: Responsibility Accounting. Authored by: Joseph Cooke. Provided by: Lumen Learning. License: CC BY: Attribution

All rights reserved content

- Responsibility Accounting. Provided by: Edspira. Located at: https://youtu.be/cwRSOKUx4rI. License: All Rights Reserved. License Terms: Standard YouTube License

- Performance Evaluation and Responsibility Centers. Authored by: Professor Coram. Located at: https://youtu.be/LdR2yOal5YA. License: All Rights Reserved. License Terms: Standard YouTube License