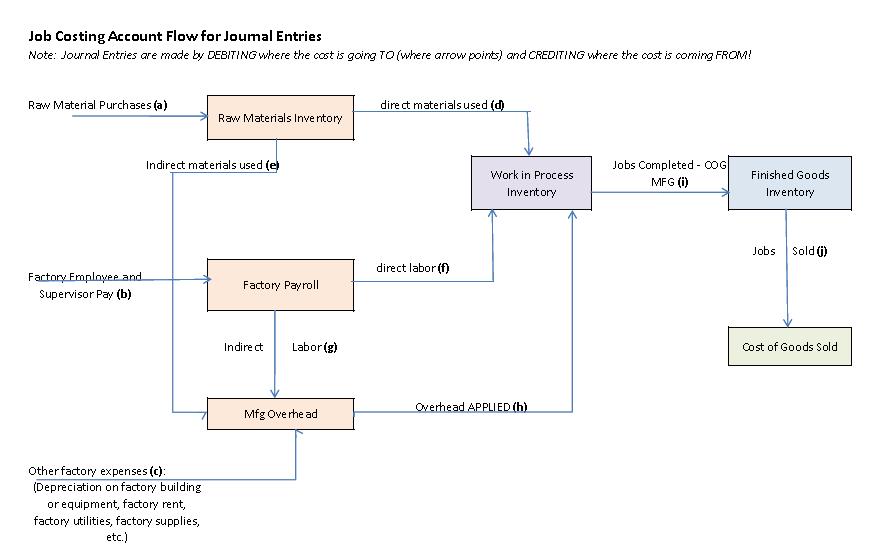

The journal entries for the flow of production costs are the same with process and job costing. The cost flow is as follows:

The corresponding journal entries to the letters in the flow chart are:

| Journal Entries by account flow (see referenced letter) | |||

| Ref | Account / Description | Debit | Credit |

| a | Raw Materials Inventory | X | |

| Cash or Accounts Payable | X | ||

| Purchased raw materials inventory | |||

| b | Factory Payroll | X | |

| Wages Payable | X | ||

| Record wages earned but unpaid | |||

| c | These are examples of some of the entries you may record: | ||

| Manufacturing Overhead | X | ||

| Accumulated Depreciation | X | ||

| Record depreciation on factory equipment | |||

| Manufacturing Overhead | X | ||

| Cash | X | ||

| Record factory rent paid with cash | |||

| Manufacturing Overhead | X | ||

| Accounts Payable | X | ||

| Record factory supplies purchased on credit | |||

| d | Work in Process Inventory | X | |

| Raw Materials Inventory | X | ||

| Record Direct Materials Used | |||

| e | Manufacturing Overhead | X | |

| Raw Materials Inventory | X | ||

| Record INDIRECT materials used | |||

| f | Work in Process Inventory | X | |

| Factory Payroll | X | ||

| Record Direct Labor | |||

| g | Manufacturing Overhead | X | |

| Factory Payroll | X | ||

| Record INDIRECT labor | |||

| h | Work in Process Inventory | X | |

| Manufacturing Overhead | X | ||

| Record Overhead APPLIED to production | |||

| i | Finished Goods Inventory | X | |

| Work in Process Inventory | X | ||

| Record jobs or goods completed (cost of goods manufactured) | |||

| j | Cost of goods sold | X | |

| Finished Goods Inventory | X | ||

| Record cost of jobs or goods completed AND sold | |||

For a printable view click job cost flow.