What you will learn to do: understand how managers direct and control decentralized operations

Well-designed performance evaluation systems offer companies many benefits. Management uses performance evaluation systems to do the following:

- promote goal congruence and coordination

- communicate critical objectives and expectations

- provide feedback to managers and thus make necessary changes to meet goals

- benchmark against industry standards

- motivate segment managers to meet expectations

This level of responsibility accounting provides reports to different levels of management. The amount of detail varies depending on the manager’s level in the organization. A performance report to a department manager of a retail store would include actual and budgeted dollar amounts of all revenue and expense items under that supervisor’s control. The report issued to the store manager would show only totals from all the department supervisors’ performance reports and any additional items under the store manager’s control, such as the store’s administrative expenses. The report to the company’s president includes summary totals of every store’s performance levels plus any additional items under the president’s control. In effect, the president’s report should include all revenue and expense items in summary form because the president is responsible for controlling the profitability of the entire company.

Management by exception is the principle that upper level management does not need to examine operating details at lower levels unless there appears to be a problem. As businesses become increasingly complex, accountants have found it necessary to filter and condense accounting data so that these data may be analyzed quickly. Most executives do not have time to study detailed accounting reports and search for problem areas. Reporting only summary totals highlights any areas needing attention and makes the most efficient use of the executive’s time.

Management by exception focuses on variances exceeding a certain dollar amount or a certain percentage. Management does not bother investigating smaller variances, since the cost would most likely outweigh the benefits.

- For cost centers, management would focus on the difference between the actual results and the flexible budget.

- For revenue centers, management would look at both the flexible budget variance and the sales volume variance.

- Profit centers are responsible for both generating revenue and controlling costs, so management would review both variances.

Condensing data for successive levels of management reports allows the appropriate manager to take the necessary corrective action and then report that to superiors without going into elaborate detail.

For example, if sales personnel costs have been excessively high in a particular department, that departmental manager should find and correct the cause of the problem. When the store manager questions the unfavorable budget variance of the department, the departmental supervisor can inform the store manager that corrective action was taken. Hence, it is not necessary to report to any higher authority that a particular department within one of the stores is not operating satisfactorily because the matter has already been resolved. Alternatively, if a manager’s entire store has been performing poorly, summary totals reported to the vice president of operations disclose this situation, and an investigation of the store manager’s problems may be indicated.

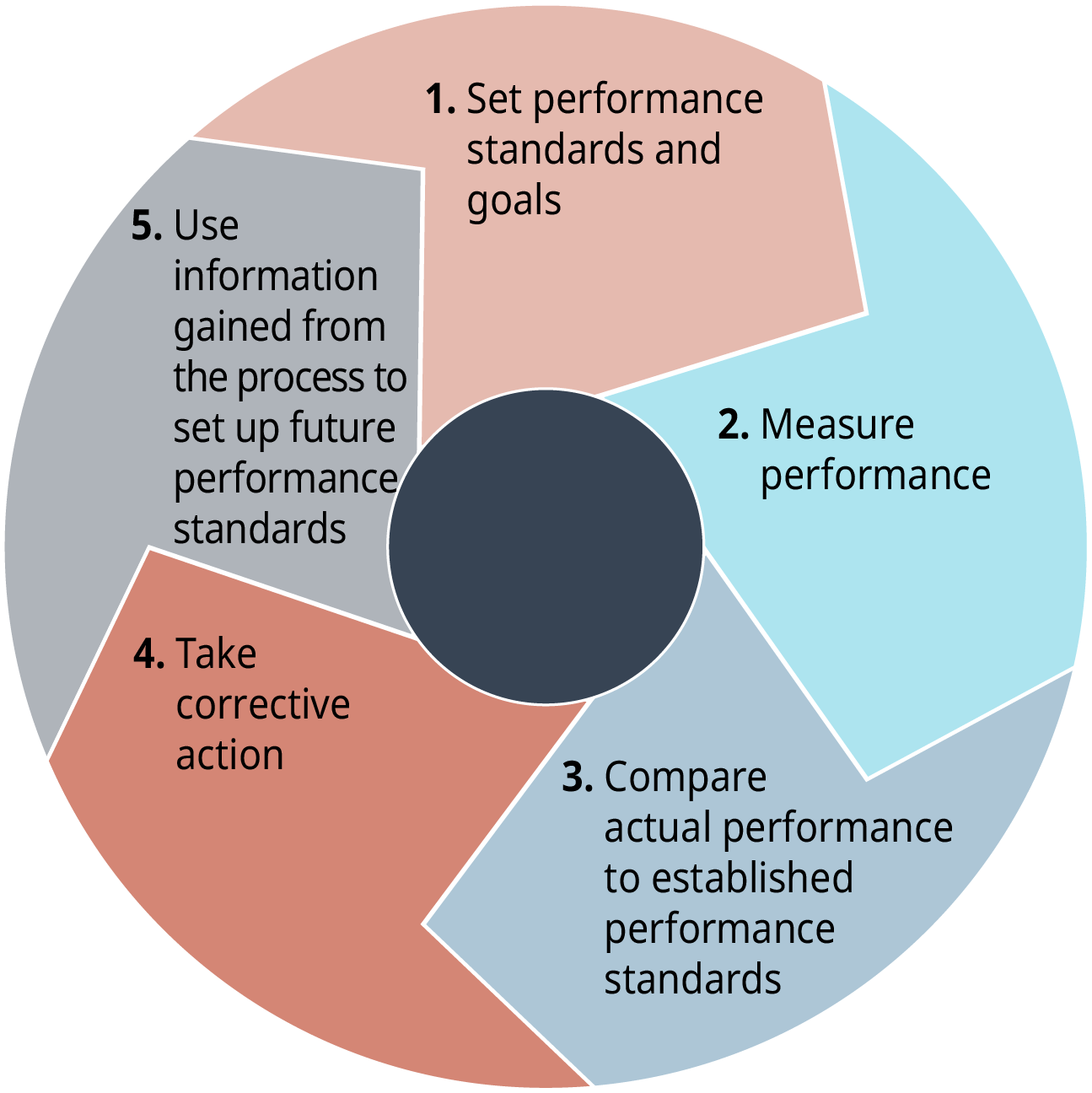

Managing performance can be visualized as a circle encompassing 5 steps:

- Set performance standards and goals

- Measure performance

- Compare actual performance to established performance standards

- Take corrective action

- Use information gained from the process to set up future performance standards

When you are done with this section, you will be able to:

- Interpret budget variances with regard to directing and controlling operations

- Identify key performance indicators for responsibility centers

- Create a balanced scorecard

Learning Activities

The learning activities for this section include the following:

- Reading: Budget Variances

- Self Check: Budget Variances

- Reading: Key Performance Indicators

- Self Check: Key Performance Indicators

- Reading: Balanced Scorecard

- Self Check: Balanced Scorecard

Candela Citations

- Introduction to Managing Performance. Authored by: Joseph Cooke. Provided by: Lumen Learning. License: CC BY: Attribution