What you’ll learn to do: Discuss different types of labor variances

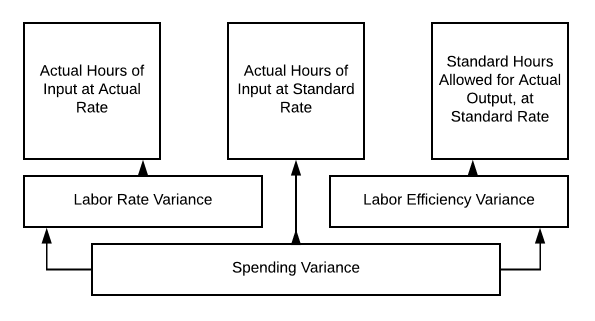

Variances in labor, like variances in materials are multifaceted. We might have the same number of hours at a different hourly rate, or more hours at the same rate, or some combination of these factors. Why would the hourly rate vary from budget? Why might the hours change? Let’s first look at the standard cost variance analysis chart for labor variances.

At Hupana Running Company, our budget allows for .5 hours of direct labor per pair of shoes produced. The cost of each hour is budgeted at $20 per hour.

If we use more hours at the same rate of pay, it would be called a labor efficiency variance.

If we used the same hours at a higher rate of pay it is called a labor rate variance.

A combination of these may happen as well! We could have fewer hours, but a higher rate of pay. Let’s see what difference these variances make in our direct labor budget!

Candela Citations

- Introduction to Labor Variances. Authored by: Freedom Learning Group. Provided by: Lumen Learning. License: CC BY: Attribution